MillerKnoll, Inc. Reports Third Quarter Fiscal 2023 Results

MillerKnoll Inc. (NASDAQ: MLKN) today reported results for the third quarter of fiscal year 2023 which ended March 4, 2023.

Business Highlights

Reported and adjusted gross margin expansion of 110 and 260 basis points respectively over the prior year.

Continued actions to reduce cost structure and improve operating efficiencies to help drive long-term margin improvement.

$123 million of run-rate cost synergies related to the Knoll integration captured to date.

Improved cash flow from operations, helping to further strengthen the balance sheet.

Third Quarter Fiscal 2023 Financial Results

*Items indicated represent Non-GAAP measurements; see the reconciliations of Non-GAAP financial measures and related explanations below.

1 In the fourth quarter of fiscal 2022 we elected to change our method of accounting for the cost of certain inventories within our Americas Segment from the last-in, first-out method ("LIFO") to first-in, first-out method ("FIFO"), which were our only operations that were using the LIFO cost method. This change was effective as of May 30, 2021. All prior periods presented have been retrospectively adjusted to apply the effects of the change.

2 The first quarter of fiscal 2023 included 14 weeks of operations as compared to a standard 13-week period. The additional week is required periodically in order to more closely align MillerKnoll's fiscal year with the calendar months.

To our shareholders:

During the third quarter of fiscal year 2023, MillerKnoll delivered strong earnings and margin expansion despite softening economic conditions. Our performance reflects the strategic management of our global operations, diverse channels and brand portfolio, and continued efforts to capture integration synergies and reduce our cost structure.

Around the globe, macro-economic factors continue to vary. Our focus on diversifying our business is allowing us to seize opportunities in new markets, introduce new products, and expand our digital capabilities to reach more customers. These actions are helping us navigate short-term macroeconomic challenges and strategically position us to capture top-line and margin improvements over the long term.

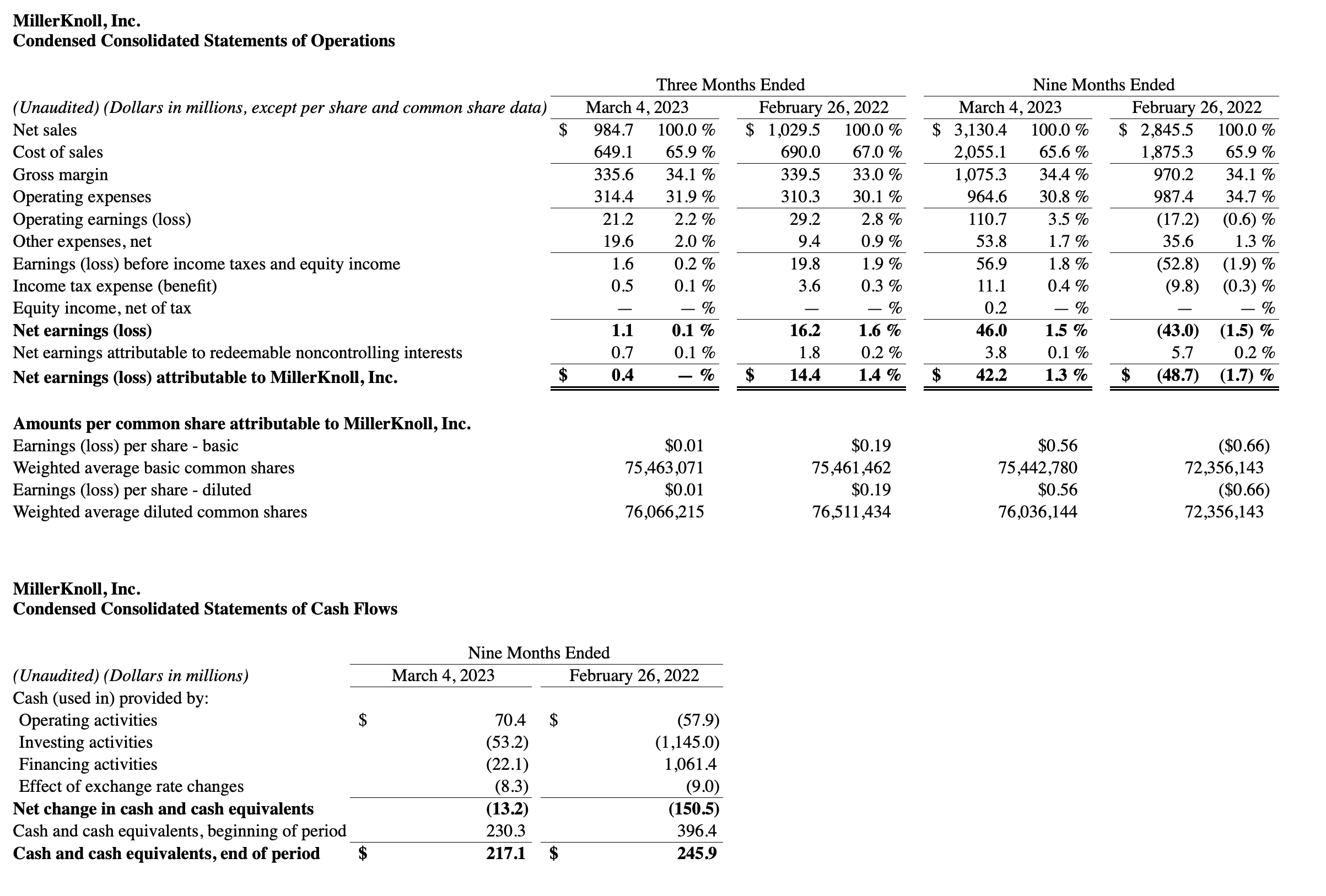

Third Quarter Fiscal 2023 Consolidated Results

Consolidated net sales for the third quarter were $984.7 million, reflecting a decrease of 4.4% on a reported basis and a decrease of 2.7% organically compared to the same period last year. Orders in the quarter of $885.4 million; were 19.2% lower on a reported basis and 17.6% lower organically versus same period last year. In addition to current economic uncertainty, prior year sales reflected an elevated pattern driven by the unwind of backlog built-up during Fiscal Year 2022. Additionally, order levels were also elevated in the previous year as a result of the initial post-COVID return to office activity, which has since slowed due to macro-economic conditions.

Gross margin in the quarter was 34.1% as reported and 35.7% on an adjusted basis, which is 110 basis points and 260 basis points higher than the same time last year, respectively. The year-over-year increase in both reported and adjusted gross margin was mainly driven by the realization of recently implemented price increases and benefits from integration synergies, which more than offset higher commodity costs and other inflationary pressures.

Consolidated operating expenses for the quarter were $314.4 million, compared to $310.3 million in the prior year. Consolidated adjusted operating expenses were $277.6 million, down $21.3 million from same time last year, primarily due to a reduction in variable compensation, further optimization of our organizational structure and cost synergies.

During the third quarter we announced targeted actions aimed at further reducing costs and improving operating efficiencies. These included the decision to cease operating Fully as a stand-alone brand and instead sell select Fully products through our Design Within Reach and Herman Miller eCommerce sites. This move will help the company reduce operating costs and further optimize its organizational structure. We believe that the ability to adjust where and how we sell products through established channels is a strong advantage of our business model, and will enable us to drive profitable growth in the long term. In total, the costs associated with the Fully brand decision and recognized in the third quarter were $37.2 million.

Operating margin for the quarter was 2.2% compared to 2.8% in the same quarter last year. On an adjusted basis, which excludes the impact of restructuring and integration-related activities described above, consolidated operating margin was 7.5% compared to 4.1% in the same quarter last year.

Diluted earnings per share were $0.01 for the quarter, compared to diluted earnings per share of $0.19 for the same period last year. Adjusted diluted earnings per share were $0.54 for the quarter, compared to $0.31 for the same period last year.

As of March 4, 2023, our liquidity position reflected cash on hand and availability on our revolving credit facility totaling $459.5 million. During the third quarter, the business generated $75.7 million of cash flow from operations and repaid $18.1 million of debt as part of our capital deployment priority of maintaining a strong balance sheet. We ended the third quarter with a net debt-to-EBITDA ratio, as defined by our lending agreement, of 2.6x. Our scheduled debt maturities for the remainder of fiscal year 2023, and for 2024, 2025, 2026 and 2027 are $6.2 million, $31.3 million, $41.3 million, $46.3 million and $276.3, million respectively.

As of the end of the third quarter, we have captured $123 million in run rate synergies following the close of the Knoll acquisition in the first quarter of Fiscal 2022. We continue to make further progress towards our target of $140 million in synergies by the end of the third year following the acquisition.

Third Quarter Fiscal 2023 Results by Segment

Americas Contract

For the third quarter, the Americas Contract segment posted net sales totaling $484.6 million, down 4.9% versus same period last year on a reported basis and down 4.5% organically. New orders in the quarter totaled $461.6 million, a decrease of 12.6% from the same quarter last year on a reported basis and down 11.8% organically. The year over year decline in orders reflects the impact of a challenging macro-economic environment compounded by pandemic-driven pent-up demand last year. Adjusted operating margin for this segment was 980 basis points higher than the same quarter last year, mainly driven by improvements from net pricing realization and incremental benefits achieved from targeted synergies. Positioning for the future, we are further enhancing our selling and digital tools to make it easier for our dealers to sell the entire MillerKnoll collective of brands while pursuing operational efficiencies and sharing best practices designed to further improve productivity and reduce costs.

International Contract and Specialty

The International Contract and Specialty segment delivered net sales in the third quarter of $242.5 million, an increase of 0.6% versus same time last year on a reported basis and up 4.3% organically. New orders in this segment totaled $210.1 million, representing a year-over-year decrease of 27.2% on a reported basis and 24.5% organically. The year over year decline in orders was mainly driven by the cycling of record post pandemic activity in the same quarter last year. This segment also delivered improved adjusted operating margin for the quarter, up 270 basis points from same time last year. The main driver of the margin expansion came from pricing actions taken earlier in the year and a favorable product mix. There is continued opportunity for the International Contract and Specialty segment as we take brands into new geographies through local accounts, particularly in the Middle East, India and Asia.

Global Retail

Net sales in the third quarter for our Global Retail segment totaled $257.6 million, a decline of 7.7% over the same quarter last year on a reported basis and down 5.5% organically. New orders in the quarter totaled $213.7 million, down 23.5% compared to the same period last year on a reported basis and down 21.3% organically. Similar to what we experienced last quarter, the decline in orders year-over-year reflect the impact of a slowdown in the North American housing market and a general increase in economic uncertainty. Orders for the quarter were also unfavorably impacted by how the timing of promotions fall within our fiscal calendar. Adjusted operating margins declined compared to last year due to a combination of lower volume, increased freight expenses and elevated inventory related costs. Notwithstanding the current economic challenges we face, we believe that the investments that we are making to expand our global reach, optimize our wholesale opportunities and better attract, understand and serve our customers are solidifying our competitive position and building additional resiliency into our retail business. Moreover, we expect these investments to position us well over the long run.

Fourth Quarter Fiscal 2023 Outlook

Around the world, our customers are navigating challenging macro-economic conditions, and we believe this will continue to put near-term pressure on our top line. Net sales for the fourth quarter of fiscal year 2023 are expected to range between $930 millionto $970 million. Adjusted diluted earnings per share are anticipated to be between $0.37 to $0.43 for the quarter.

Driving Growth Through Product Innovation, Inclusive and Sustainable Design

Across our collective of brands, we continue to innovate by launching new products within all our brands and through all our channels. In addition, we continue to deliver against our sustainability goals. During this quarter, Herman Miller was recognized by The Chemical Footprint Project for our commitment to minimizing chemical footprints and integrating criteria for better alternatives into our design and safety processes.

We are aware that this is a period of disruption. Nevertheless, with a diversified business that serves many sectors and fosters a culture of innovation and collaboration, we believe that we are well positioned for growth and expansion. Moreover, disruption brings changes and opportunities. As MillerKnoll, we envision and design the solutions with and for our customers, we have superior brands and an unmatched product portfolio, and we are expanding our distribution through a combination of contract and retail channels. We believe this is a powerful formula for a strong future.