Steelcase Reports Third Quarter Fiscal 2023 Results

Steelcase Inc. reported third quarter revenue of $826.9 million, net income of $11.4 million, or $0.10 per share, and adjusted earnings per share of $0.20. In the prior year, Steelcase reported revenue of $738.2 million and net income of $9.6 million, or $0.08 per share, and had adjusted earnings per share of $0.11.

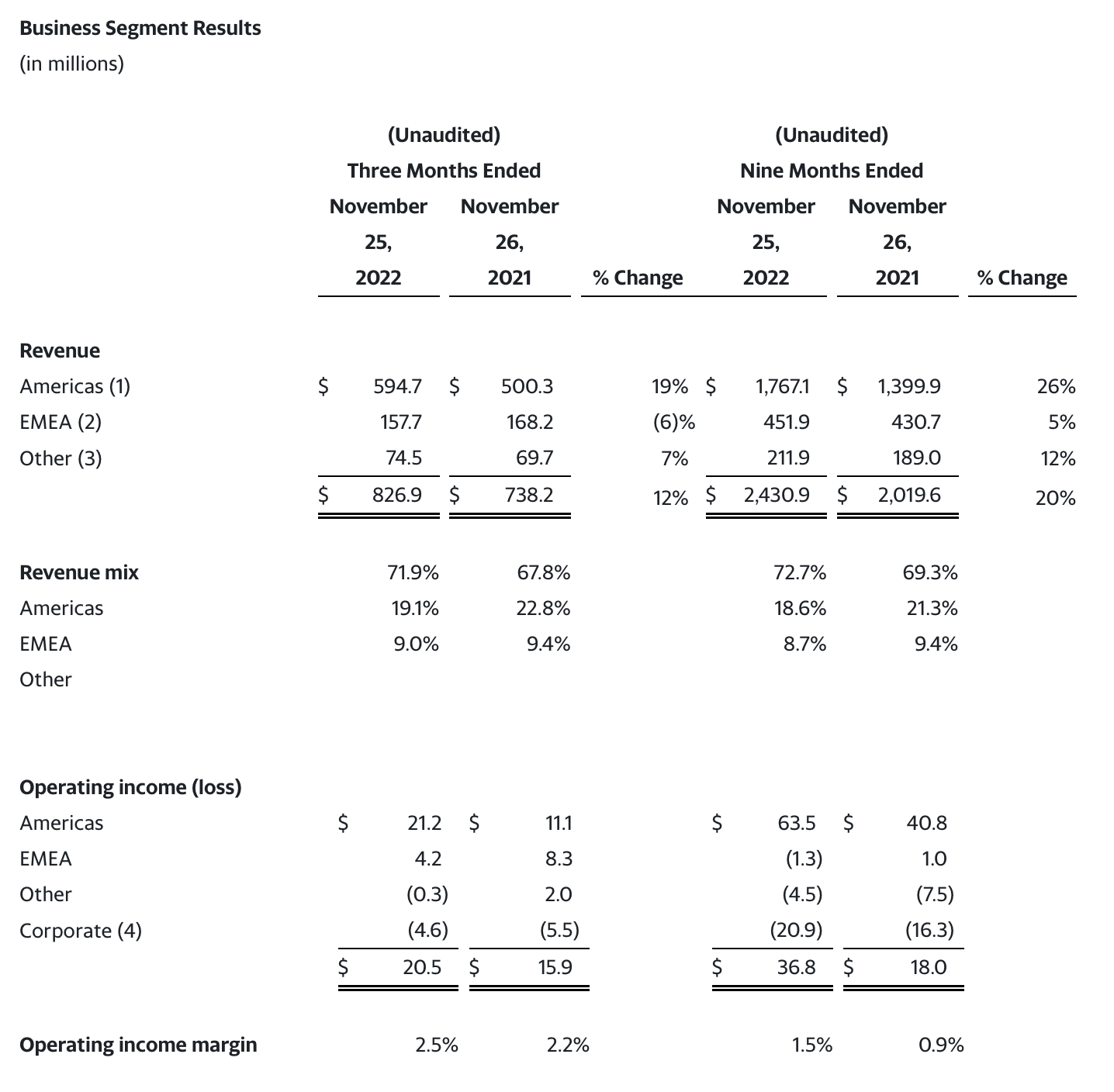

Revenue and order growth (decline) compared to the prior year were as follows:

The organic revenue growth in all segments was driven by a strong beginning backlog and included significant pricing benefits. Orders declined across all segments, with a decline in volume partially offset by pricing benefits. Orders were impacted by softening industry demand patterns believed to be driven by reduced sentiment related to growing macroeconomic and geopolitical concerns. The order decline in the Other category was additionally impacted by COVID-related restrictions in China and reflected an overall decline in Asia Pacific compared to growth of more than 100 percent in the prior year.

"We delivered revenue and earnings growth this quarter that met our expectations in a challenging environment," said Sara Armbruster, president and CEO. "I'm proud of how our teams maintained their focus on implementing price increases in response to significant inflation, mitigating the impact of supply chain disruptions and controlling our level of spending."

Operating income (loss) and adjusted operating income (loss) were as follows:

Operating income of $20.5 million in the third quarter represented an increase of $4.6 million compared to the prior year. Adjusted operating income of $37.7 million in the third quarter (which excludes $10.6 million of restructuring costs and $6.6 million of amortization of purchased intangible assets) represented an increase of $18.2 million compared to the prior year. The increase in adjusted operating income was primarily driven by higher pricing benefits, net of inflation, partially offset by higher operating expenses.

Gross margin of 28.8 percent in the third quarter represented an increase of 120 basis points compared to the prior year, and reflected a 280 basis point improvement in the Americas, a 240 basis point decline in EMEA and a 230 basis point decline in the Other category. Year-over-year pricing benefits of approximately $85 million exceeded year-over-year inflation by approximately $55 million. The improvement in the Americas was primarily due to higher pricing benefits, net of inflation, and higher volume, partially offset by higher fixed overhead costs and labor inefficiencies. The decline in EMEA was primarily due to freight and labor inefficiencies, unfavorable currency impacts and the impact of lower volume. The decline in the Other category was primarily due to higher inflation, net of pricing benefits, and unfavorable currency impacts.

"Our gross margin improvement in the Americas this quarter reflected the benefits from the pricing actions we've been implementing in the face of extraordinary inflation levels," said Dave Sylvester, senior vice president and CFO. "On a global basis, year-over-year pricing benefits have exceeded year-over-year inflation for the last two quarters; however, we estimate cumulative inflation over the last seven quarters exceeds the cumulative benefits from our pricing actions by approximately $60 million. Moving into the fourth quarter and first half of fiscal 2024, we expect continued year-over-year gross margin benefits from our pricing actions, as we aim to recover the cumulative impact of inflation."

Operating expenses of $208.1 million in the third quarter represented an increase of $20.4 million compared to the prior year. The increase was driven by $14.9 million of higher variable compensation expense, $8.1 million from acquisitions and $3.4 million of higher marketing, product development and sales expenses, partially offset by $5.9 million of favorable currency translations effects.

"During the third quarter, we implemented our previously announced actions to reduce headcount in the Americas and Corporate, and we recently initiated actions to wind down our aviation department and sell our aircraft," said Dave Sylvester. "We recognized restructuring costs in the third quarter related to the headcount reductions and expect to recognize approximately $3 million of additional restructuring costs in the fourth quarter of 2023 related to the wind down of aviation. We estimate approximately $30 million of annualized savings from these actions and we expect to use the proceeds from the sale of our aircraft to pay-off the related financing, which matures in the first quarter of fiscal 2024."

Interest expense of $7.6 million in the third quarter represented an increase of $1.1 million compared to the prior year due to borrowings under the company's global credit facility.

Total liquidity, comprised of cash and cash equivalents and the cash surrender value of company-owned life insurance, aggregated to $216.2 million at the end of the third quarter. Total debt was $516.0 million. Adjusted EBITDA for the trailing four quarters was $177.0 million.

The Board of Directors has declared a quarterly cash dividend of $0.10 per share, to be paid on or before January 13, 2023, to shareholders of record as of January 3, 2023.

Outlook

At the end of the third quarter, the company’s backlog of customer orders was approximately $854 million, which was 3 percent higher than the prior year. Consistent with recent quarters, the backlog includes a higher than historical percentage of orders scheduled to ship beyond the end of the next quarter. Orders through the first three weeks of the fourth quarter declined approximately 6 percent compared to the prior year. As a result, the company expects fourth quarter fiscal 2023 revenue to be in the range of $740 to $765 million. The company reported revenue of $753.1 million in the fourth quarter of fiscal 2022. The projected revenue range is approximately flat, including on an organic basis, compared to the fourth quarter of fiscal 2022.

The company expects to report earnings per share of between $0.05 to $0.09 for the fourth quarter of fiscal 2023 and adjusted earnings per share of between $0.11 to $0.15. The estimates include:

gross margin of approximately 29 percent, with projected pricing benefits, net of inflation, of approximately $65 million as compared to the prior year,

projected operating expenses of between $195 to $200 million, which includes $6.5 million of amortization of purchased intangible assets and $10 million of expected gains from the sale of fixed assets,

estimated restructuring charges of approximately $3 million,

projected interest expense, investment income and other income, net, of approximately $5 million and

a projected effective tax rate of 28 percent.

The company reported a loss per share of $0.02 and had breakeven adjusted earnings per share in the fourth quarter of the prior year.

“The needs of people at work are changing profoundly,” said Sara Armbruster. "As our customers enhance their workspaces, we remain focused on bringing them solutions that inspire and support better ways of working. We believe our strategy to lead the hybrid transformation, diversify the customers and markets we serve, and increase our profitability will drive improved financial results and stronger shareholder returns."